Income Tax for Non-Residents (IRNR)

There is an optional category for IRNR (Impuesto sobre la renta de los No Residentes) taxpayers who meet the following requirements:

- They are natural persons who can prove they are resident in another EU Member State, except residents of countries or territories considered by the regulations to be non-cooperative tax jurisdictions, or in an EEA Member State with which there are regulations on mutual assistance relating to the exchange of tax information.

- Regarding their income:

- At least 75 per cent of their entire income in the tax period is income from work and economic activity earned during that tax period in Spanish territory, or

- They can prove that the income earned during the financial year in Spain was below 90 per cent of the minimum personal and family threshold that would have corresponded to them on the basis of their personal and family circumstances had they been resident in Spain. in addition, that the income earned outside of Spain also fell below that threshold.

You can find the regulation in the Official Website: BOE: Official State Gazette, Royal Legislative Decree 5/2004, of March 5, approving the revised text of the Non-Resident Income Tax Law.

Income obtained in Spain

Exception case applicable to any type of income : Income is not considered to be earned in Spain in some cases:

- paid to non-resident persons or organisations,

- by permanent establishments located abroad,

- at their own expense,

- when the corresponding services rendered are directly linked to the activity of the permanent establishment abroad.

Double Tax Agreement vs IRNR

When there is a Double Taxation Agreement (DTA) with a country, the DTA is applied, meaning the international regulation. The purpose of the DTA, which often follows the OECD model, is to allocate taxing rights between jurisdictions. If the DTA grants taxing rights to Spain, the Non-Resident Income Tax (IRNR) will be applied. However, if the agreement assigns taxing rights to the other jurisdiction, Spain will not be able to impose taxes, even if the IRNR considered a taxable event.

In the absence of a DTA, domestic regulations will apply, in this case, the IRNR.

Tax rates for income tax for non-residents

| Concept | Tax Rate |

|---|---|

| General Basis | 24% |

| Income from work (seasonal workers) | 2% |

| Dividends and other returns from entity’s own funds Interest and other income from capital transfer Capital gains from collective investment institutions Other capital gains from asset transfers | 19% |

| Pensions and other similar benefits | See scale below |

Pension Taxation Scale

| Annual Pension Amount (up to euros) | Fee (euros) | Rest of Pension (up to euros) | Applicable Rate (%) |

|---|---|---|---|

| 0 | 0 | 12,000 | 8% |

| 12,000 | 960 | 6,700 | 30% |

| 18,700 | 2,970 | above | 40% |

Beckham Law or Inpatriate Law

Option to be taxed under the Non-Resident Income Tax (IRNR), while maintaining the status of taxpayers under the Personal Income Tax (IRPF), during the year of the change of residence and the following five years, when the following conditions are met:

- Not having resided in Spain in the previous five years.

- Moving to Spain for one of the following reasons:

o Moving to Spain due to a work contract.

o Becoming an administrator of a company.

o Undertaking entrepreneurial activities in Spain.

o Providing services as qualified personnel to start-up companies.

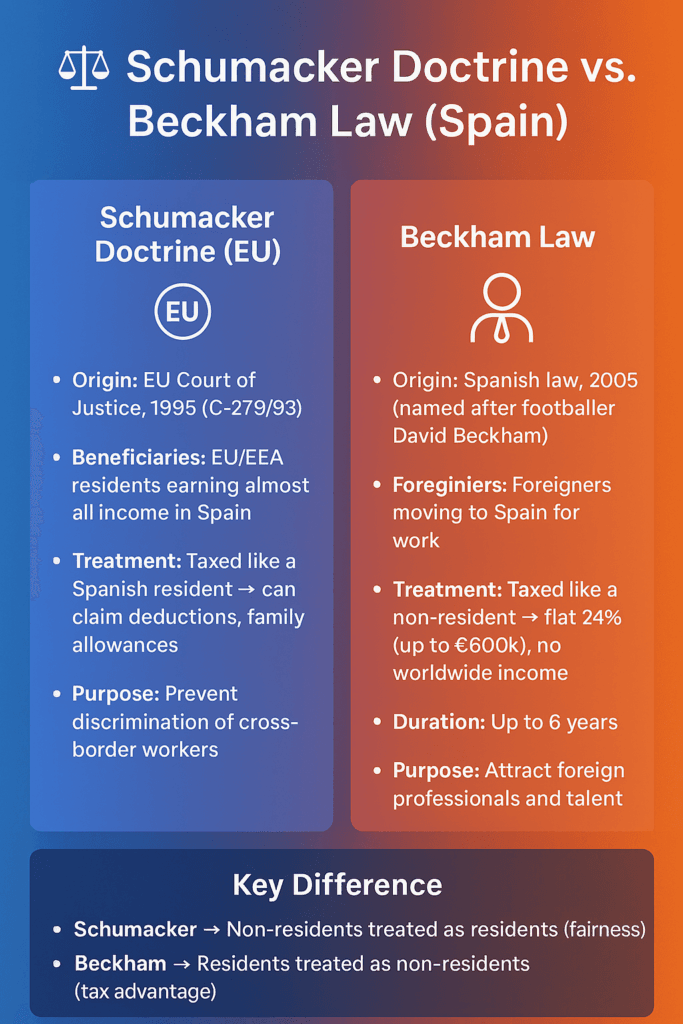

💼 Beckham Law (Spain’s “Régimen fiscal de impatriados”)

- Origin: Spanish tax reform in 2005, nicknamed after footballer David Beckham when he moved to Real Madrid.

- Concept: A special tax regime for foreigners moving to Spain for work.

- How it works:

- You are treated as a non-resident for tax purposes, even while living in Spain.

- Pay a flat 24% (up to 600k €) / 47% (above) tax rate only on Spanish income (worldwide income is excluded).

- Valid for up to 6 years.

- Goal: Attract highly skilled workers and talent to Spain.

Main charateristics of Beckam Law

The regime is characterized by allowing individuals who acquire residence in Spain as a result of their relocation to choose to be taxed under Non-Resident Income Tax (IRNR) while maintaining their status as Personal Income Tax (IRPF) contributors. It also implies being subject to the real obligation in the Wealth Tax.

These taxpayers, despite being residents in Spain, are not taxed on their worldwide income in Spain. They are only taxed on income sourced from Spain, at the rates and under the rules of the IRNR without a permanent establishment (PE).

This territorial taxation is the reason, for example, that the current Double Taxation Agreement (DTA) with Germany states that this DTA does not apply to those who choose this expatriate regime.

It has also been noted in consultations from the Directorate General of Taxes (DGT) that those opting for this regime will not be considered residents for the purpose of applying a DTA signed by Spain.

This regime can only be applied during the period in which residence is acquired and the following five years.

Extra Perks

An extra perk, apart from the low rate:

- Withholding percentage up to 600,000 euros: 24%

- Withholding percentage from 600,001 euros: 47%

It is called the Beckham Law because soccer player David Beckham was the first to benefit from this law when he signed with Real Madrid. In more technical terms, Article 93 of the Personal Income Tax Law (IRPF) applies.

Schumacker Case for EU Residents

This regime originates from Recommendation 94/79 of the Commission dated December 21, 1993, resulting from various rulings by the Court of Justice of the European Union (CJEU), such as the Schumacker ruling on February 14, 1995. It is a clear example of how a Recommendation (soft law) and the CJEU indirectly achieve the harmonization, or at least approximation, of the legislation of countries in the area of direct taxation, as discussed in Topic 2.

This regime is characterized by allowing a resident in the EU who meets certain requirements to be taxed as if they were a resident.

The requirements to opt for this regime are as follows:

- The taxpayer must be an individual resident for tax purposes in a territory of the EU that is not classified as a tax haven.

- Establishing a domicile or habitual residence in an EU Member State.

- That at least 75% of their total income comes from employment and economic activities carried out in Spain, or that the income earned during the fiscal year in Spain has been less than 90 percent of the personal and family minimum that would have applied if they had been a resident in Spain, and that the income earned outside Spain has also been below that minimum.

- That they choose to be taxed under the Personal Income Tax (IRPF), provided that they have effectively paid taxes during the period under Non-Resident Income Tax (IRNR).

⚖️ Schumacker Doctrine (EU Law)

- Origin: European Court of Justice case C-279/93 Schumacker (1995).

- Concept: An EU worker who earns most or all of their income in another EU country should be treated like a resident for tax purposes there.

- In Spain:

- If you live in another EU/EEA country but earn almost all your income in Spain, you can request to be taxed as a Spanish resident.

- This allows you to claim deductions, allowances, and family benefits that normally only residents can.

- Goal: Prevents discrimination against cross-border workers.

Main characteristics of Schumacker Law

- All income earned in Spain is subject to taxation (net income).

- The tax rate is the average rate of the IRPF, taking into account their worldwide income (not just Spanish income) and personal circumstances.

Taxpayers do not lose their status as non-resident income tax (IRNR) contributors (e.g., they will be subject to withholding by the buyer in the case of a property sale).

The taxpayer declares under the IRNR, and once the application of the regime is verified, the tax authorities determine the amount of IRPF and refund any excess.

The justification for this regime lies in the principle of non-discrimination and equity, according to which equal treatment must be given to those in similar circumstances. The Schumacker ruling and the EU Recommendation understood that when a non-resident earns more than 75% of their income in a country different from their residence, they find themselves in the source country under circumstances similar to those of a resident in that same source country, and therefore should be taxed similarly.

In other words, the non-resident should have access to deductions and tax benefits that take their personal circumstances into account, such as, in the Spanish case, the tax-exempt minimum and the family minimum.

Schumacker Law vs Beckam Law

These are two very different legal concepts in Spain, though they sometimes get confused because both deal with taxation and foreigners.

🔑 Key Differences

| Aspect | Schumacker | Beckham Law |

|---|---|---|

| Type | EU Court doctrine | Spanish national law |

| Who benefits | Non-residents working mainly in Spain (cross-border EU/EEA workers) | Foreigners who move their tax residence to Spain for work |

| Treatment | Treated like a resident → can claim deductions | Treated like a non-resident → flat tax, no worldwide income |

| Purpose | Prevent discrimination | Attract expats and talent |

| Example | A Portuguese living in Portugal but working 90% in Spain | A UK executive relocating to Madrid for 5 years |

👉 In short:

- Schumacker = fairness for cross-border EU workers.

- Beckham = tax incentive for foreign professionals moving to Spain.